July 29, 2024

Flooding is by far the most common, costly, and destructive natural disaster in the United States, causing billions in economic losses each year. According to the Federal Emergency Management Agency (FEMA), flooding causes 90% of disaster damage every year.

Everyone is at risk for flood damage, regardless of location. Given the increasing prevalence and risk of flooding, homeowners should take a fresh look at their flood risks and consider how flood insurance can be incorporated into their overall risk management and insurance strategy.

National Oceanic and Atmospheric Administration (NOAA) confirms — flooding causes more damage than any other type of weather event in the US and can occur in all 50 states, any time of year. Floods are occurring more frequently, even in areas and states that haven’t historically experienced them.

From 2000-2020, the amount the National Flood Insurance Program (NFIP) paid in flood insurance claims increased by a staggering 660%. In the years to come, many more properties will sustain damage from floods and other natural disasters as the frequency of extreme weather events continues to increase.

Despite the risks, however, flood insurance remains a largely untapped form of protection. Since 1996, 99% of counties in the U.S. have experienced a flood, but only 4% of homeowners have flood insurance.

Surprisingly, many property owners often lack flood insurance coverage because they either assume flood coverage is already included in their standard homeowner's policy, or they assume their property is not at risk for flooding. While homeowner's insurance policies typically cover water damage from things like burst pipes, leaks, and broken water heaters, these policies do not cover flood damage resulting from heavy rainfall, storm surges, melting snow, or other natural storms or events.

Many homeowners also greatly underestimate the risk, feeling they do not need flood insurance in their geographic location. This could be a costly mistake. Over 40% of the National Flood Insurance Program’s (NFIP) claims come from outside high-risk flood zones. Additionally, extreme weather and climate changes are making increased rainfall and flooding more common and more severe, causing floods in areas that are not historically prone to them.

Here's a breakdown of the types of coverage that can be included in a flood insurance policy. However, it is important to note that there are different types of flood policies and not all policies offer the same coverages or limits. Your specific needs should be discussed with your insurance broker to ensure proper flood coverage and adequate limits are in place.

Protects the structure of your home, including walls, floors, foundation, electrical and plumbing systems, furnaces and water heaters, built-in appliances (refrigerators, ovens, stoves, dishwashers), permanent carpeting, window blinds, detached garages, attached fixtures like cabinets, fuel tanks, well water tanks and pumps, and solar energy equipment. FEMA NFIP policies specifically outline these as covered:

Coverage options differ between FEMA NFIP and private flood insurance policies.

Flood insurance is a powerful protection tool, but it has its limitations. It's always best to consult with your insurance broker to ensure your policy covers everything you need it to, and to understand any exclusions that might apply. Here's what typically falls outside the scope of a flood insurance policy:

Flood insurance doesn't cover internal plumbing issues like burst pipes (and resulting water damage).

Items not covered by building or contents coverage (on a FEMA NFIP policy), but may be covered by some private flood policies:

There are two primary sources for flood policies, the National Flood Insurance Program (NFIP) and the Private Market. Given the increased frequency and risk of flood damage, homeowners need to understand the various flood insurance types that exist within the marketplace, as well as the pros and cons of each.

FEMA (Federal Emergency Management Agency) manages and administers the National Flood Insurance Program (NFIP), which enables property owners to purchase insurance against losses from flooding at a reasonable cost. The National Flood Insurance Program (NFIP) is delivered to the public by a network of more than 50 insurance companies and the NFIP Direct.

Since the NFIP is intended for disaster relief, the coverage is base-level, does not include extra coverages such as loss-of-use, has many exclusions, and has limit caps. Other factors to consider:

Private flood coverage is written by insurance companies that are not part of the federal government flood program. In recent years, more carriers have entered the private flood insurance marketplace.

Factors to consider when choosing Private Flood Insurance coverage. If you’re looking for custom flood insurance that can be tailored to your specific needs, you may want to explore private flood insurance. The private market addresses a lot of the gaps in FEMA flood insurance policies.

Excess flood insurance policies cover over – in excess of – primary flood insurance policies. Layering coverage involves combining a primary policy such as a NFIP policy or private flood policy, with an excess flood policy. Excess policies can extend over NFIP policies or over private flood insurance policies.

For high-value homes, excess flood insurance can be a wise option to consider as it offers higher limits than primary flood insurance, especially if covering over an NFIP flood policy, which only covers up to $250,000 for the dwelling and $100,000 for personal property. If your property value or contents significantly exceed standard flood insurance limits, excess flood coverage can bridge the gap and provide additional financial protection.

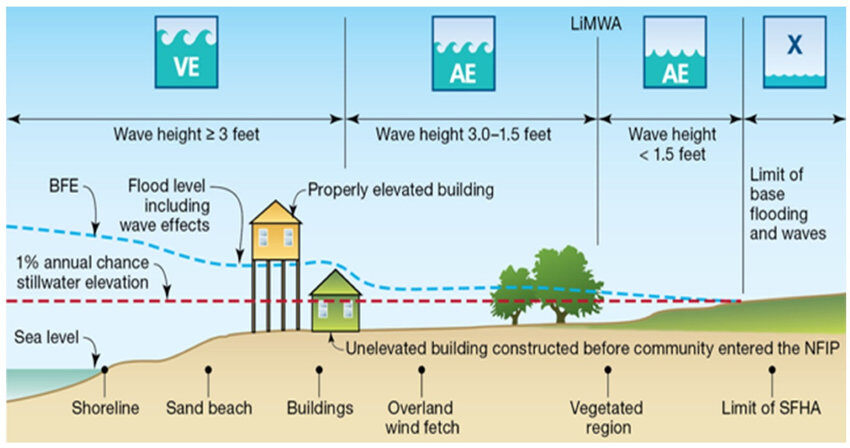

Understanding your property's Flood Zone and location on a Flood Map are crucial flood safety steps. FEMA creates Flood Insurance Rate Maps (FIRMs) that designate flood risk areas across the country. The highest flood hazard areas identified on the Flood Insurance Rate Maps are identified as part of the Special Flood Hazard Area.

In the illustration above, the dashed red line represents a 1% inundation level and the dashed blue line is the base flood elevation (BFE). These can be referenced to grade elevation. Zone definitions are provided at the top of the figure (VE, AE, LIMWA, and X).

Ilustration credit: Spaulding, Malcolm & Grilli, Annette & Damon, Chris & Hashemi, Reza & Kouhi, Soroush & Fugate, Grover. (2020). Stormtools Design Elevation (SDE) Maps: Including Impact of Sea Level Rise. Journal of Marine Science and Engineering. 8. 292. 10.3390/jmse8040292.

The SFHA is defined as an area having special flood, mudflow or flood-related erosion hazards and shown on a Flood Hazard Boundary Map (FHBM) or a Flood Insurance Rate Map (FIRM) as Zone A or Zone V, including Zones AO, A1-A30, AE, A99, AH, AR, AR/A, AR/AE, AR/AH, AR/AO, AR/A1-A30, V1-V30, VE or V. The SFHA is the area where the National Flood Insurance Program's (NFIP's) floodplain management regulations must be enforced and the area where the mandatory purchase of flood insurance applies.

Flood Zone V is located in the SFHA and includes coastal areas with a 1% or greater chance of flooding and an additional hazard associated with storm waves. Flood insurance is mandatory for federally backed mortgages in this zone.

Flood Zone A is located in the SFHA and there is a 1% annual chance of flooding and a 1 in 4 chance of flooding during a 30-year mortgage. Flood insurance is mandatory for federally backed mortgages in this zone.

Flood Zone D indicates areas with possible but undetermined flood hazards. No flood risk analysis has been conducted for these areas. Flood insurance is not mandatory, but it may still be recommended due to the potential for flooding.

Flood maps are subject to change due to weather patterns and development. Regularly checking your flood zone status ensures you have the appropriate coverage and a full understanding of your risk. Consult your insurance broker for help interpreting the flood map and determine your specific flood risk. FEMA's Flood Map Service Center allows you to search for your property's flood zone by address.

Floods affect more people around the globe than any other disaster. Even if you live far from the ocean, a river, or other water features, you may find yourself in damaging flooding scenarios. Floods come in many forms. Three flood types pose a risk to homes:

Proactive steps can significantly reduce flood damage to your home, regardless of location. The following protective measures can make a big difference and enhance your flood preparedness. However, these steps are just the beginning. Consulting with a flood mitigation specialist and your insurance broker can help identify additional measures specific to your property and flood risk.

Homeowners need to be aware of increasing flood risks and understand the flood insurance options available to them. While flooding risks are typically highest in coastal and waterfront areas in flood-prone states, all states and properties have some degree of flood risk and exposure.

With the frequency, severity, and cost of flooding events expected to increase continually, all homeowners should include flood insurance coverage in their risk management program. Review all your insurance policies annually with a private client specialist to ensure you have the right coverage in place.