2023 State of the Market - Business Insurance

Coverage Considerations

2022 proved to be a banner year in the captive insurance industry. There was a broader adoption of captive solutions with an increasingly more sophisticated mid-market clientele.

As we look further into 2023, there appears to be some easing of commercial premiums in challenging markets (Cyber liability, Directors & Officers, etc). Despite this easing, many clients who are serious about risk management and loss control are continuing to place a meaningful amount of retention in their captives. Businesses with a larger employee base who self-fund their group medical benefits are also writing a layer of the stop loss insurance in their own captive with much more frequency. Oftentimes, there is a level of potential underwriting profit that can be retained over time by using a captive for a portion of the medical stop loss.

As we look further into 2023, there appears to be some easing of commercial premiums in challenging markets (Cyber liability, Directors & Officers, etc). Despite this easing, many clients who are serious about risk management and loss control are continuing to place a meaningful amount of retention in their captives. Businesses with a larger employee base who self-fund their group medical benefits are also writing a layer of the stop loss insurance in their own captive with much more frequency. Oftentimes, there is a level of potential underwriting profit that can be retained over time by using a captive for a portion of the medical stop loss.

As businesses explore the benefits of captives to provide their own risk financing solutions, there has been a meaningful uptick in the use of a captive as a profit center providing insurance backing to warranty programs, tenant damage and security deposit waivers, self-storage contents protection, and the like. When well run, these captives offer a revenue stream complementary to the core business. As the captive grows in size, the business has more options in the amount of risk they can retain. The most sophisticated clients are writing multiple lines of coverage through their captive to maximize the utility.

Recommendations

Clients should start by becoming more knowledgeable about how captives are structured and how they can help them manage risk, no matter the size of their business. From there, they:

- Develop a list of major causes of loss which can adversely impact revenue

- Identify those insurance programs which are commercially available and those which are not

- Retain risk management consultant(s) for guidance on possible ways to address these risks

- Conduct a feasibility study to determine the expected return on investment of a captives program

- Consider retention of risk and other techniques to develop the most cost-effective program

"When well run, these captives offer a revenue stream complementary to the core business."

Industry Insights

2022 saw a return to a more competitive and nuanced market than in the previous three years. The casualty market for many businesses was varied and dynamic. Overall, competition for business grew from its previous levels.

2022 saw a return to a more competitive and nuanced market than in the previous three years. The casualty market for many businesses was varied and dynamic. Overall, competition for business grew from its previous levels.

The casualty market has truly become a “tale of two cities.” Companies with good loss experience, reasonably sized vehicle fleets with exceptional loss control, who operate in low-to-moderate hazard classes of business, achieved good results in 2022. However, several industries continue to face headwinds: habitational real estate, transportation, education, certain nonprofits, certain retailers, and those that operate in jurisdictions known as “judicial hellholes” have fared considerably worse.

In 2023, insurers will be concerned about emerging and negative casualty claims trends stemming from:

- “Forever chemicals” and other hazardous chemicals and materials. Without detailed underwriting information, clients with potential exposure to these and other hazardous materials will face exclusions in their general liability policies.

- Sexual abuse exposure. Institutions with sexual abuse exposures will continue to struggle with obtaining sufficient coverage. Several states, most recently Maine, have amended their laws to adjust the plaintiff’s ability to bring or reopen claims well beyond previous statutes of limitations, even claims over 30 years old.

- Increase in workers’ compensation risks. The Great Resignation and the recent hesitation to hire needed staff given the economic challenges could lead to an increase in workers’ compensation claims from insufficient and overworked staff. New cases are arising from musculoskeletal disorders from poorly designed home workstations. The NCCI reports that loss ratios are rising again. That said, we do not anticipate that underwriters will seek significant premium increases in 2023.

- Social inflation from TPLF. Verdicts continue to exceed the inflation rate. One increasing cause is third-party litigation funding (TPLF), which allows those who previously were unable to bear legal fees to shift that cost to a third party. In return, the third party receives a substantial portion of the settlement. Thus, insurers are seeing more lawsuits and larger settlements. Insurers are now facing an ongoing battle against well-funded opportunists, willing to take cases further for potentially larger settlements.

Coverage Considerations

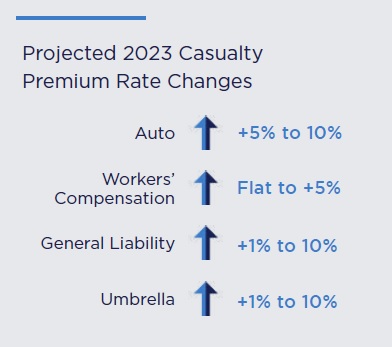

As we look at 2023, the Casualty market is expected to experience rising premiums, but at much lower levels compared to recent results. However, there are substantial differences by line of coverage, industry, and size of company that will ultimately determine what each individual client pays.

Underwriters continue to face the same issues as in 2022 such as inflation, rising claim costs, and nuclear verdicts. Further concerns with the reinsurance market eased somewhat based on casualty treaty renewals as of January 1, suggesting at least three to six months of stability for many primary insurers. As 2023 progresses, a crucial concern will be the ongoing availability of reinsurance at a reasonable price for Casualty insurers, given the substantial pressure being put on the property reinsurance market.

Recommendations

- Monitor inflation and its effect on many areas of the economy, such as labor costs, auto parts, litigation, and construction. Businesses may be reflecting higher revenue figures but with flat or lower unit sales.

- Consider using unit volume as your general liability exposure basis (instead of revenue) to offset the potential impact of inflation on their premium.

- Analyze any increase in workers’ compensations claims to understand root causes. Are new hires receiving adequate safety training? Is a team short-staffed, resulting in more overtime? Both fatigue and inexperience can lead to accidents.

Industry Insights

Ransomware attacks and other cyber threats have spiked considerably in recent years. When cyberattacks lead to data breaches, organizations are left vulnerable to litigation, making these issues costly to resolve. Because ransomware attacks have also led to massive extortion payouts, cybercriminals have become emboldened, driving increases in ransom demands.

Ransomware attacks and other cyber threats have spiked considerably in recent years. When cyberattacks lead to data breaches, organizations are left vulnerable to litigation, making these issues costly to resolve. Because ransomware attacks have also led to massive extortion payouts, cybercriminals have become emboldened, driving increases in ransom demands.

These criminals have also exploited the rapid shift to remote work brought on by the COVID-19 pandemic. As many organizations rushed to implement work-fromhome capabilities, their IT systems were left vulnerable while they worked to put effective security measures in place.

The increasing prevalence of attacks has caused more stringent underwriting review and robust requirements for security controls. Clients with a favorable loss history and sufficient controls like multi-factor authentication (MFA) should be able to minimize rate increases and coverage limitations, while those lacking controls or with paid or open claims in their history may be unable to secure adequate coverage.

Coverage Considerations

We are finally entering a period of greater stability as 2023 progresses after several years of increased frequency and severity of claims inflating premiums. Insurers took significant corrective action over the last couple of years and pricing is now at a point where long-term profitability can be maintained.

Additionally, underwriting discipline and focus on controls has resulted in better behavior across the market and a material reduction in claims frequency and severity.

Additionally, underwriting discipline and focus on controls has resulted in better behavior across the market and a material reduction in claims frequency and severity.

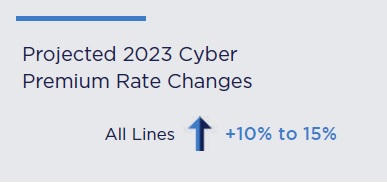

There are still rate increases, but they are more modest, averaging 20% in Q4 2022. Some clients are still experiencing more severe increases, such as those with inferior controls, but for clients with strong controls and favorable loss experience, there is more pricing consistency year over year.

Insurers remain focused on the quality of risk and are working to further refine their policy language to manage their exposure to a potential systemic event that could trigger losses portfolio-wide.

Coverage Considerations

Competition continues to be aggressive in the environmental space. Businesses should expect relatively flat rate increases of 0% to 7% in 2023 as a result.

Environmental carriers are seeing an increase in environmental insurance placements driven by emerging issues. Environmental insurance, once a discretionary buy for risk managers, is now part of an overall risk management strategy.

Claims expenses are on the rise in certain geographies. Older cities with properties containing lead, asbestos, and chlorinated solvents have been a significant source. As well, wind, flooding, and fire spread the effects of environmental events by moving the contamination from the source area to other sites.

Carriers’ appetites for difficult environmental risks remain strong. However, because of emerging issues, increased trends in claims, and social inflation, underwriters require comprehensive and complete information when underwriting the risk.

It is expected that carriers will attempt to exclude PFAS on new and renewal business and raise deductibles in areas where they have experienced an increase in claims in certain industries groups or cannot demonstrate that a company has not been impacted by the use of PFAS.

Recommendations

To minimize the likelihood of environmental hazard claims, it is essential to develop a robust environmental risk management strategy.

- Identify any potential exposures and put the necessary measures in place to ensure environmental safety to both mitigate risks and protect the business from costly claims.

- Perform due diligence to determine whether any of their operations or products contain PFAS chemicals. If those companies are part of an industry group that has historically used PFAS in operations, they likely will be facing exclusions unless they can demonstrate a way to mitigate liabilities through indemnities.

- During an acquisition buy/sell transition, it is crucial to take the necessary steps to ensure that the company’s environmental impact is thoroughly evaluated.

- Conduct a baseline assessment which will provide a comprehensive overview of the organization’s environmental impact and any related potential risks.

"Environmental insurance, once a discretionary buy for risk managers, is now part of an overall risk management strategy."

Industry Insights

The international property hard market continues as the January 1 reinsurance renewals proved to be as challenging as the market has seen in decades. By comparison, January 1 casualty reinsurance renewals were much less volatile.

Property reinsurers were impacted by Hurricane Ian and other CAT activity in 2022. In addition, the continued impact of inflation, supply chain disruption, and the war in Ukraine resulted in another challenging year from a loss perspective.

As a result, reinsurers looked to recoup loss costs through rate increases, increased retentions, and in some cases, changes in terms and conditions. While most reinsurers softened their position on the terms and conditions changes, many were successful on the rate and attachment fronts as demand in many cases outstripped supply.

The reinsurance market aside, even in an elevated rate environment where new capacity has entered the market, underwriting discipline has remained relatively consistent which has significantly limited any potential market softening.

Industry Insights

The accelerated downturn in the directors and officers (D&O) and management liability space has continued into 2023. Clients and customers are experiencing rate reductions mirroring what we saw at the end of 2022 as the soft market continues.

Macroeconomic Environment

The challenging macroeconomic environment will continue to put increased financial pressure on clients, which will temper the improved pricing environment stemming from the influx of new capacity. The temporary COVID-19 economic shutdown has been replaced by inflation. This has led to increased risk of bankruptcies and layoffs. Companies need to take aggressive actions to manage profitability, all of which will impact how carriers will price their business and the limits they will deploy on a given risk.

The challenging macroeconomic environment will continue to put increased financial pressure on clients, which will temper the improved pricing environment stemming from the influx of new capacity. The temporary COVID-19 economic shutdown has been replaced by inflation. This has led to increased risk of bankruptcies and layoffs. Companies need to take aggressive actions to manage profitability, all of which will impact how carriers will price their business and the limits they will deploy on a given risk.

Loss cost inflation, especially in the public D&O space, continues to rise. It is uncertain what the final impact will be on carrier balance sheets once all the securities class action claims filed right before and during the pandemic settle.

The total amount of securities class action settlements was $7.4 billion in 2022, a 75% increase from 2021. Insurance carriers funded a portion of those settlements and the ultimate impact on balance sheets for this business line remains to be seen.

SEC & ESG

Environmental, Social Risks, and Governance (ESG) disclosure and reporting requirements are one of those areas in the SEC’s line of sight. The increase in ESG-related requirements necessitates that companies understand and address relevant challenges. Diversity, Equity, and Inclusion (DE&I) issues continue to impact D&O — in particular, Employment Practices Liability (EPLI) exposures. Equal pay and compensation-related claims are on the rise. Failing to address ESG could lead to derivative claims, shareholder claims, and accusations of breach of fiduciary duties by D&O.

Coverage Considerations

The market is in transition from a hard to a soft market, but it is facing headwinds from a challenging economic environment, the financial impact of COVID-19, continued high inflation, and an industry that has seen a significant uptick in loss costs that are impacting carrier profitability.

The degree of transition varies by line of business and industry segment. The new capacity that came into the market in the past three years had an impact on right-sizing the supply/demand equation, ultimately leading to much more favorable pricing and expanded policy terms. This new capacity will continue to favorably impact the market in 2023, especially on programs with excess limits.

As compared to 2022, there will be continued increased competition across all lines of business. Legacy carriers have remediated their books in the past few years and are now focused on retaining accounts; particularly against newer market entrants.

Unlike the first part of 2022 when the IPO market — specifically SPACs – was robust, that market has since evaporated. Thus, there is less net new business in the market for carriers to target. Coupled with the new capacity that entered the market in the past three years, the market should benefit buyers with attractive risk profiles and little to no significant claims activity.

Buyers will benefit in terms of reduced premiums, lower SIRs, stable or increased limits capacity, and expanded coverage terms.

Some risks that may not realize the same pace of rate deceleration will be:

- IPOs and SPACs

- Clients with bankruptcy or liquidity challenges

- Specific industry classes, such as Life Science, Cannabis, Retail, Cryptocurrency, Financial Institutions, and Retail

Industry Insights

At the start of last year, many industry experts predicted hard market conditions would ease in 2022. That was not to be. Eighteen weather- and climate-related events resulted in total losses exceeding $150 billion, including $60 billion from Hurricane Ian losses in Florida and South Carolina. The property insurance and reinsurance markets quickly reacted. All clients have been impacted especially those with locations prone to named wind/storm surge events. They have seen significant reductions in coverage capacity, as well as higher deductibles, rates, and premiums.

At the start of last year, many industry experts predicted hard market conditions would ease in 2022. That was not to be. Eighteen weather- and climate-related events resulted in total losses exceeding $150 billion, including $60 billion from Hurricane Ian losses in Florida and South Carolina. The property insurance and reinsurance markets quickly reacted. All clients have been impacted especially those with locations prone to named wind/storm surge events. They have seen significant reductions in coverage capacity, as well as higher deductibles, rates, and premiums.

The market continues to refine its underwriting position on secondary perils such as tornadoes, floods, wildfires, hailstorms, and freeze. Some underwriters are taking a hardline approach and excluding coverages, while others are establishing high deductibles for locations prone to these loss types. Underwriters may also restrict tornado and hailstorm coverage on roofs based on conditions and age.

Global reinsurance capacity dropped significantly in 2022 evidenced by the results of the property risk and catastrophe reinsurance January 1 renewal season. Those treaties hit by catastrophic (CAT) losses in 2022, in particular Hurricane Ian, saw rate increases of 100% or more with reinsurance programs coming together at the last minute. While most insurers were able to source enough capacity, it came at higher costs and attachment points. Last-minute negotiations made it difficult for insurers to give clear direction to the field on what their treaty renewals looked like in January and what it would mean for their clients.

April 1 is another critical treaty renewal period. It may prove to be tougher than January 1 as reinsurers have a clearer picture on 2022 results and what they need to be profitable in 2023.

Coverage Considerations

Many clients with January 1 renewals may have missed the full impact of Treaty changes. The burden now falls on those accounts that renew after January 1. Some new capacity entered the market capitalizing on better pricing and terms but not enough to slow the market down.

For all but wood frame/joisted construction projects, the builders risk market is still competitive. Favorable pricing, terms and conditions, and capacity are readily available for high-quality construction projects in the non-CAT retail market. The excess & surplus (E&S) market responds well to frame/joisted projects. Both retail and E&S markets respond well to mass timber/cross laminated timber projects.

Water damage losses continue to grow in size and frequency in construction projects as well as existing high-rise, healthcare, multifamily, and other buildings. Underwriters are imposing higher water damage deductibles and reducing water damage limits. They are even mandating the purchase and installation of water detection devices for early alerts of water leakage.

Underwriters continue to have limited appetites for certain occupancy types such as food, habitational, wood products, and recycling operations. Deals come together at a cost with lower limits and higher deductibles.

A recent building appraisal analysis showed that nearly 90% of buildings appraised in 2020 and 2021 were undervalued. As a result, 68% of buildings were underinsured by 25% or more and 19% were underinsured by 100%. Underwriters continue to focus on the adequacy of replacement cost values amidst inflation, higher labor and material costs, and supply chain issues. Underwriters may look for building and contents value increases as high as 10-20%, which translates to higher insurance premiums.

Unless clients take steps to increase their property values to today’s dollars, underwriters will impose coinsurance, remove blanket occurrence limits of liability, and apply limits per location among other things. Claims adjustments can be difficult too if the loss measurement is higher than values reported at a location.

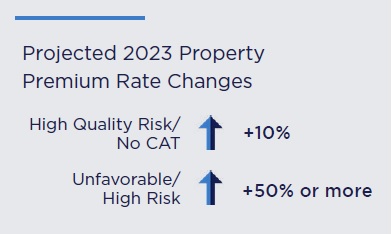

Rate disparity between good risks without CAT and poor risks with CAT will continue in 2023. Good quality risks without CAT exposures and losses will see rate increases, on average of 10% while poor risks with CAT and with loss experience will see increases of 50% or more.

Industry Insights

The U.S. Surety market thrived in 2022.

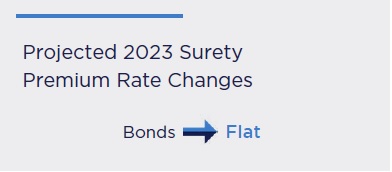

Construction grew approximately 10%, while sureties showed continued profitability and low loss activity. With additional capacity derived from established and new providers, a relatively soft surety market continues.

With that tailwind, there are also headwinds for construction in 2023. Construction, and by extension the surety market, are lagging indicators of the overall economy. The past few years’ tremendous growth and demand coupled with significant supply and labor challenges, low interest rates, and government-assisted cash infusions led to rampant inflation. These rising costs have taken a toll on many contractors’ balance sheets.

With that tailwind, there are also headwinds for construction in 2023. Construction, and by extension the surety market, are lagging indicators of the overall economy. The past few years’ tremendous growth and demand coupled with significant supply and labor challenges, low interest rates, and government-assisted cash infusions led to rampant inflation. These rising costs have taken a toll on many contractors’ balance sheets.

This financial strain, along with project delays and cancellations and tightening credit markets, resulted in softening business conditions during the 2022 fourth quarter. These factors will likely continue to stress the construction industry during the first half of 2023. The AIA’s Architecture Billings Index fell below the meaningful “50” threshold in October of last year, further indicating headwinds over the next six to nine months.

The Infrastructure Bill will begin adding projects into the public space in earnest in 2023. Nearly all labor for the bill is provided throughout the construction industry. This boost to the construction landscape will also put additional pressure on contractors to hire, train, and retain new talent.

These dynamics will put strain on construction lenders as well to maintain strong cash balances and debt ratios on their balance sheets while proactively managing material and personnel to be prepared for economic challenges. Contractors also have more backlog to support with their Surety bond programs. That could lead to difficulty getting new bonds unless the balance sheet is healthy. With the new headwinds, the current soft market may become a bit harder.

Coverage Considerations

The Surety market is still relatively soft, driven by sufficient reinsurance capacity and new surety companies entering the market. The real challenges for contractors are keeping their balance sheet robust and having the staff and resources to perform well and clear out the backlog. Bids from early 2022 are already seeing profit erosion from the inflationary effects and high interest rates.

Surety bond underwriters are going to look closely at contractors’ ability to fix a problem before it becomes a claim and their ability to not take on more projects than they can manage well.